The global industrial sector is witnessing a significant transformation in safety management practices as companies increasingly prioritize explosion prevention, operational continuity, and regulatory compliance.

At the heart of this transformation lies the growing adoption of flame and detonation arrestors—critical safety devices designed to prevent flame propagation and explosion-related incidents in hazardous industrial environments.

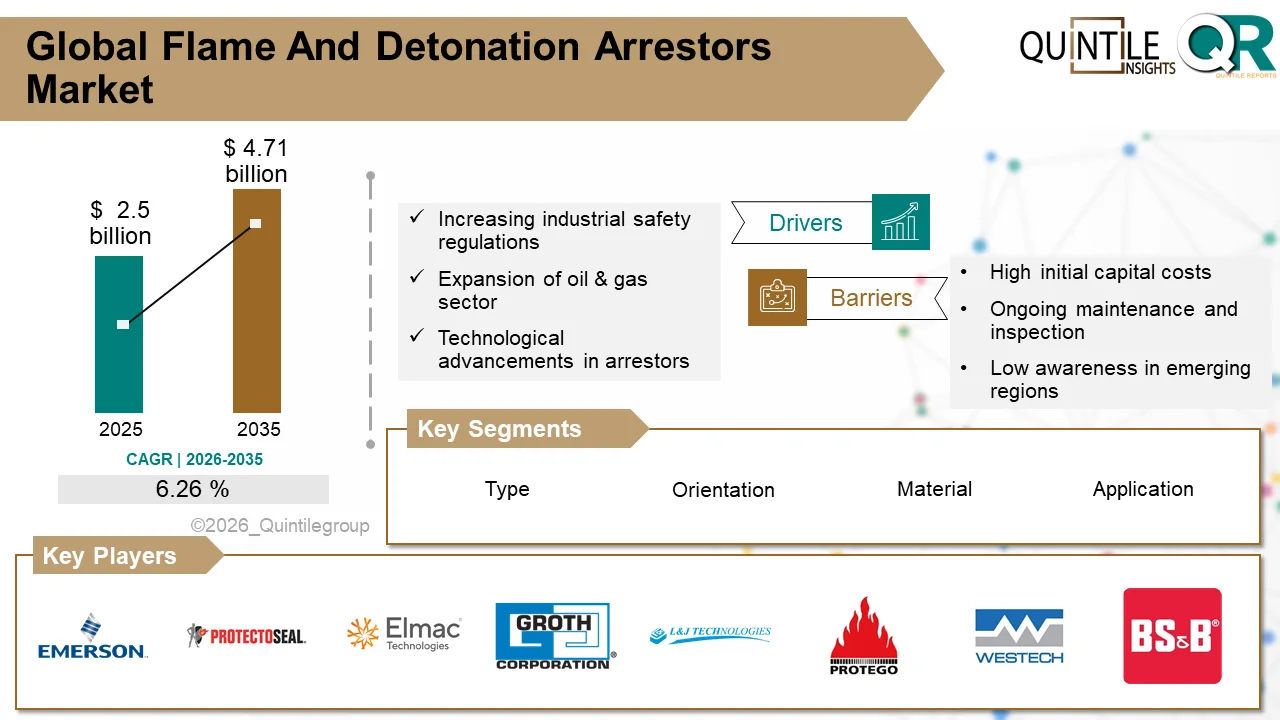

According to recent industry analysis, the global Flame and Detonation Arrestors Market was valued at USD 2.61 billion in 2026 and is projected to reach USD 4.71 billion by 2036, expanding at a compound annual growth rate (CAGR) of 6.26% during the forecast period.

The market’s growth reflects the increasing need for advanced industrial safety systems across oil and gas, petrochemical, chemical processing, power generation, pharmaceutical manufacturing, mining, and other high-risk industries where flammable gases and volatile substances are routinely handled.

Request Sample PDF Report: https://www.quintilereports.com/request-sample/1293-flame-and-detonation-arrestors-market/

Growing Focus on Explosion Prevention

Industrial explosions continue to pose significant risks to personnel, infrastructure, and the environment. As industrial processes become more complex and production facilities expand, companies are investing heavily in technologies that can reduce operational risks while ensuring compliance with stringent safety regulations.

Flame and detonation arrestors serve as passive protection devices that prevent flames, combustion waves, and detonation shock fronts from traveling through pipelines, vents, tanks, and process equipment. These devices utilize specially engineered flame-quenching elements that absorb heat and extinguish flames before they can propagate into critical areas.

Their ability to provide reliable protection without requiring external power sources makes them indispensable in facilities handling combustible gases, vapors, and volatile chemicals.

Discount Now: https://www.quintilereports.com/request-discount/1293-flame-and-detonation-arrestors-market/

With governments and regulatory agencies tightening industrial safety requirements, flame and detonation arrestors are rapidly becoming standard equipment across numerous industrial applications.

Regulatory Compliance Driving Market Expansion

One of the most important factors supporting market growth is the implementation of increasingly strict industrial safety regulations worldwide.

Organizations operating in hazardous environments must comply with standards designed to prevent workplace accidents and minimize explosion-related risks. Regulatory frameworks such as ATEX directives in Europe, NFPA guidelines in North America, and various national industrial safety standards are compelling companies to adopt certified explosion prevention technologies.

Failure to comply with these regulations can result in substantial financial penalties, operational shutdowns, reputational damage, and increased liability exposure.

As a result, many industrial operators view flame and detonation arrestors not merely as safety devices but as strategic investments that protect assets, personnel, and long-term business continuity.

The emphasis on compliance is particularly strong in sectors where flammable gases and liquids are stored, processed, or transported through extensive infrastructure networks.

Oil and Gas Industry Remains a Major End User

The oil and gas sector continues to represent one of the largest application areas for flame and detonation arrestors.

From upstream exploration and production facilities to downstream refining and storage operations, the industry relies heavily on explosion protection systems to safeguard critical infrastructure.

Storage tanks, vapor recovery systems, flare stacks, gas processing facilities, and transportation pipelines all require reliable flame arresting solutions to prevent fire and explosion incidents.

The expansion of oil and gas infrastructure projects across North America, the Middle East, Asia-Pacific, and Latin America is generating substantial demand for advanced arrestor technologies.

In the United States, increasing investments in shale oil and gas development are creating new opportunities for safety equipment suppliers. Expanding pipeline networks, processing facilities, and storage terminals require sophisticated protection systems capable of meeting stringent federal safety standards.

Similarly, energy-rich nations in the Middle East are investing heavily in refinery modernization and infrastructure expansion, further supporting market growth.

Buying Now: https://www.quintilereports.com/request-enquiry/1293-flame-and-detonation-arrestors-market/

Technological Innovation Enhances Performance

Manufacturers are continuously improving arrestor designs to meet evolving industrial requirements and operational challenges.

Recent technological advancements have significantly enhanced the efficiency, durability, and reliability of modern flame and detonation arrestors. Improvements in flame-quenching technology, thermal management systems, corrosion-resistant materials, and modular installation designs are helping end users achieve higher safety performance while reducing maintenance requirements.

One of the most notable developments is the integration of digital monitoring capabilities into explosion protection systems.

IoT-enabled arrestors can provide real-time performance monitoring, predictive maintenance alerts, and operational diagnostics, allowing facility managers to identify potential issues before they impact safety or productivity.

These smart technologies align with broader industrial digitalization initiatives and support predictive maintenance strategies increasingly adopted across manufacturing and process industries.

Chemical and Petrochemical Industries Accelerate Adoption

The chemical and petrochemical sectors are also contributing significantly to market expansion.

These industries frequently handle highly flammable materials and operate under stringent safety requirements. The presence of volatile gases, reactive chemicals, and combustible vapors makes explosion prevention a top operational priority.

Flame and detonation arrestors are widely deployed in storage facilities, processing units, reactor systems, transfer lines, and venting applications to mitigate risks associated with ignition sources and flame propagation.

As global demand for chemicals, specialty materials, and petrochemical products continues to grow, manufacturers are investing in new production facilities and upgrading existing assets with modern safety systems.

These investments are expected to generate sustained demand for advanced arrestor technologies throughout the forecast period.

Infrastructure Modernization Creates New Opportunities

Aging industrial infrastructure presents another important growth opportunity for market participants.

Many facilities built decades ago were designed under different safety standards and often require modernization to comply with current regulations.

Operators are increasingly retrofitting existing systems with upgraded explosion prevention equipment to improve safety performance and reduce operational risks.

The modernization trend extends beyond developed economies. Emerging markets are also investing heavily in industrial infrastructure development and adopting international safety standards as part of broader industrialization initiatives.

Countries such as China, India, Brazil, and Saudi Arabia are expanding refinery capacity, chemical production facilities, and energy infrastructure, creating favorable conditions for flame and detonation arrestor suppliers.

Regional Growth Trends

North America Maintains Leadership Position

North America remains one of the most mature markets for flame and detonation arrestors due to its well-established industrial base and stringent regulatory environment.

The United States continues to lead regional demand, supported by robust investments in energy infrastructure, petrochemical production, and industrial safety upgrades.

OSHA regulations and NFPA standards continue to drive widespread adoption across multiple industries.

Europe Strengthens Safety Compliance

Europe maintains a strong market position through rigorous implementation of ATEX directives and advanced industrial safety practices.

Countries such as Germany, the United Kingdom, and the Netherlands continue to invest in explosion protection technologies for chemical processing plants, biogas facilities, refineries, and manufacturing operations.

The region’s emphasis on operational safety and environmental responsibility further supports market expansion.

Asia-Pacific Emerges as Fastest-Growing Region

Asia-Pacific is expected to experience the fastest growth during the forecast period.

Rapid industrialization, increasing energy demand, expanding petrochemical capacity, and growing awareness of workplace safety are driving adoption across China, India, Japan, and Southeast Asia.

Governments throughout the region are strengthening industrial safety regulations while encouraging modernization of manufacturing infrastructure.

These initiatives are creating substantial opportunities for both domestic and international arrestor manufacturers.

Challenges Facing the Market

Despite strong growth prospects, the industry faces several challenges.

High installation and maintenance costs remain a barrier, particularly for small and medium-sized enterprises operating under budget constraints.

The technical complexity of selecting, installing, and maintaining arrestors also requires specialized expertise, which may not always be readily available in emerging markets.

Another challenge involves regulatory complexity. Certification requirements vary significantly across regions and industries, increasing compliance costs for manufacturers and end users.

Additionally, operational factors such as corrosion, particulate buildup, thermal cycling, and harsh process conditions can impact long-term performance if maintenance practices are not properly implemented.

Addressing these challenges will require ongoing innovation, education, and collaboration among manufacturers, regulators, and industrial operators.

Competitive Landscape Evolves

Competition within the Flame and Detonation Arrestors Market is increasingly centered on innovation, technical expertise, and integrated safety solutions.

Leading companies are investing in research and development to create products with enhanced performance characteristics, longer service life, and digital monitoring capabilities.

Manufacturers are also expanding service offerings to include installation support, predictive maintenance programs, remote diagnostics, and turnkey safety system integration.

Strategic acquisitions and partnerships continue to reshape the competitive landscape. Industry participants are pursuing opportunities to strengthen global distribution networks, expand technological capabilities, and improve customer support infrastructure.

The market remains moderately consolidated, with established global players competing alongside specialized regional manufacturers that focus on niche applications and localized service delivery.

Future Outlook

Looking ahead, the Flame and Detonation Arrestors Market is expected to benefit from continued industrial expansion, regulatory enforcement, and growing awareness of explosion prevention strategies.

The integration of smart monitoring technologies, advanced materials, and predictive maintenance capabilities will further enhance the value proposition of modern arrestor systems.

As industries increasingly prioritize risk management, environmental protection, and operational resilience, flame and detonation arrestors will remain essential components of industrial safety infrastructure.

With global market value projected to approach USD 4.71 billion by 2036, the sector is positioned for steady and sustainable growth driven by technological innovation, infrastructure investment, and the universal need for safer industrial operations.

1. What is the projected market size of the Flame and Detonation Arrestors Market by 2036?

The market is expected to reach USD 4.71 billion by 2036, growing at a CAGR of 6.26%.

2. What are flame and detonation arrestors used for?

They prevent flame propagation, explosions, and detonation shock waves in pipelines, storage tanks, vents, and industrial processing systems.

3. Which industries are the largest users of flame and detonation arrestors?

Major end-use industries include oil & gas, petrochemicals, chemicals, pharmaceuticals, power generation, mining, and waste-to-energy facilities.

4. What is the difference between a flame arrestor and a detonation arrestor?

Flame arrestors stop low-speed flame propagation, while detonation arrestors are engineered to withstand and stop high-pressure detonation shock waves.

5. What factors are driving market growth?

Key drivers include stricter industrial safety regulations, expansion of oil & gas infrastructure, increased explosion prevention requirements, and advancements in arrestor technology.

6. Which region currently dominates the market?

North America leads the market due to strong regulatory enforcement, extensive energy infrastructure, and high adoption of industrial safety systems.

7. Why is Asia-Pacific expected to grow rapidly?

Rapid industrialization, petrochemical expansion, infrastructure investments, and strengthening safety regulations are driving demand across Asia-Pacific.

8. How is IoT influencing flame and detonation arrestor technology?

IoT-enabled systems provide real-time monitoring, predictive maintenance, performance diagnostics, and enhanced operational safety.

Our Latest Publication:

Flame and Detonation Arrestors Market (2026-2036)

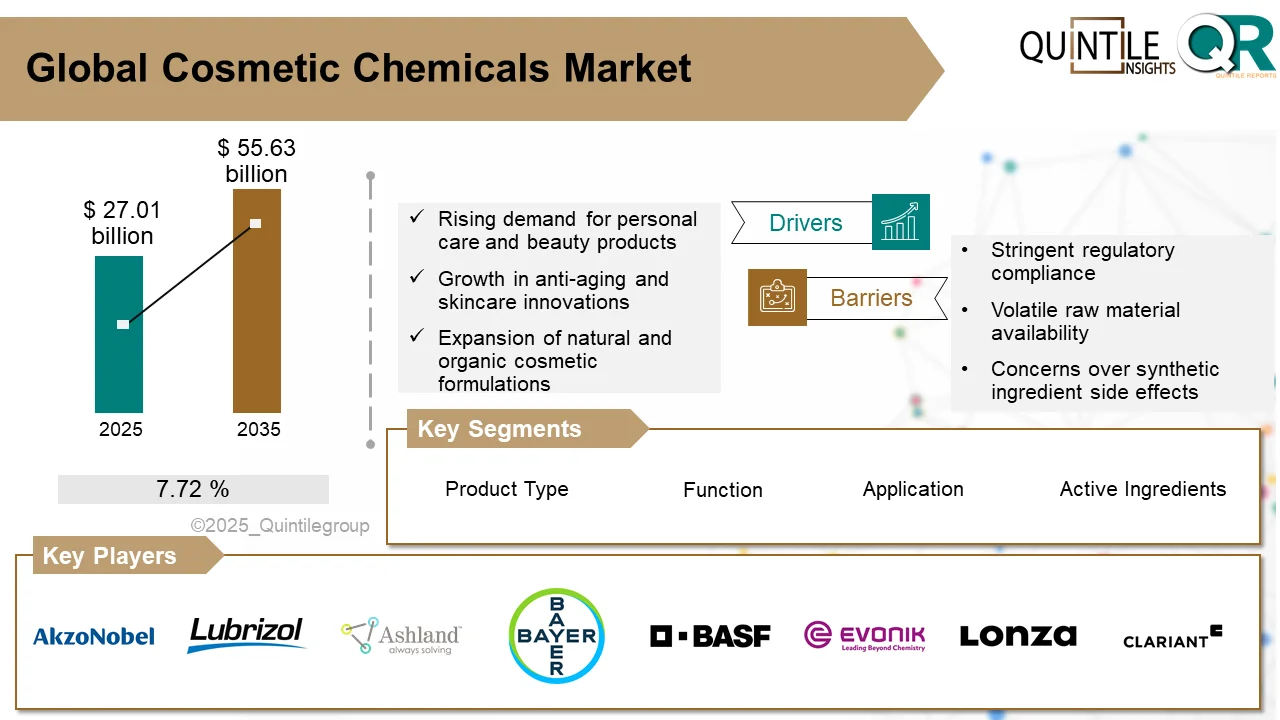

Cosmetic Chemicals Market Toward USD 55.63 Billion by 2035

Adarsh

Business Strategy — Quintile Reports

Adarsh is a Business Strategy professional focused on transforming market insights into actionable growth plans. He supports strategic initiatives through market analysis, competitive intelligence, and data-driven decision-making to help drive long-term business success.

His core skills include strategic planning, market research, growth opportunity assessment, trend analysis, performance tracking, stakeholder communication, cross-functional collaboration, and critical problem-solving.