The global Non-GMO Flour Market is witnessing sustained expansion as consumers increasingly prioritize transparency, natural ingredients, and clean-label food products.

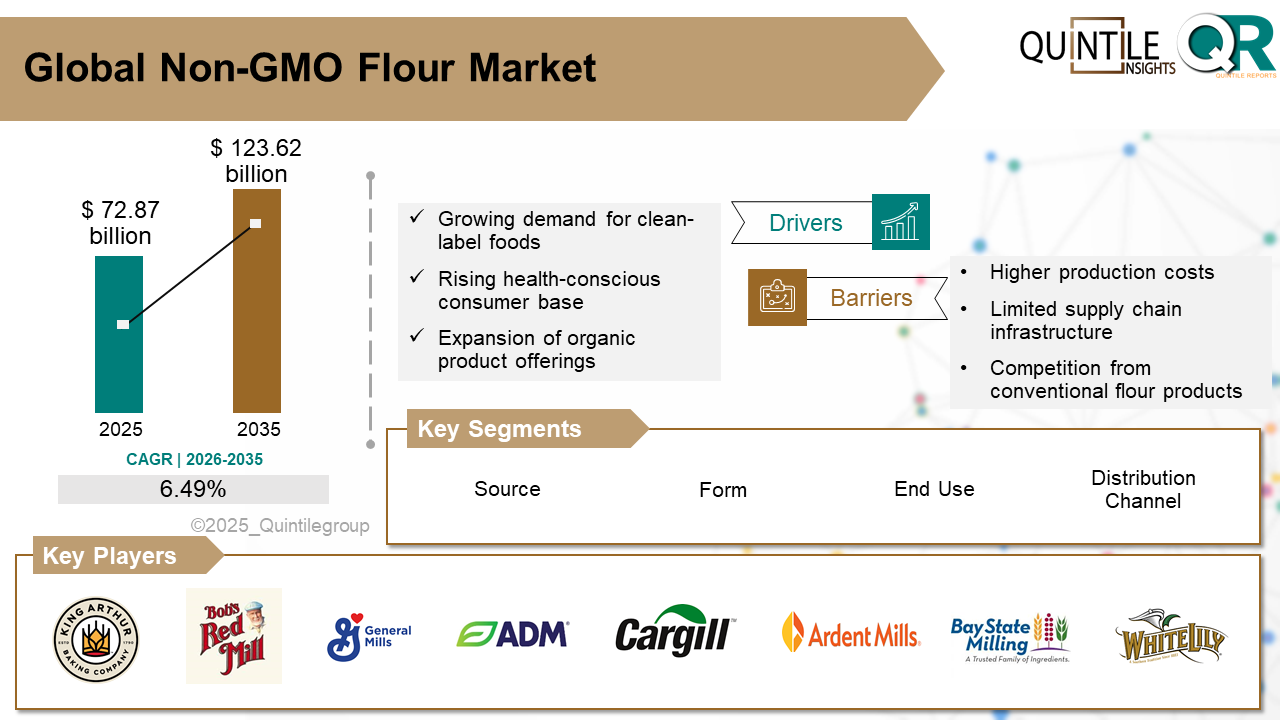

Valued at USD 72.87 billion in 2025, the market is projected to reach USD 123.62 billion by 2035, growing at a compound annual growth rate (CAGR) of 6.49% during the forecast period from 2026 to 2035. This growth reflects a broader shift in global food consumption patterns toward minimally processed and responsibly sourced ingredients.

Non-GMO flour is produced from grains that have not been genetically modified through laboratory-based genetic engineering. Instead, these grains are cultivated using conventional breeding methods, aligning with growing consumer concerns around food safety, environmental sustainability, and ingredient authenticity. Certification programs such as the Non-GMO Project play a crucial role in validating product claims, strengthening consumer confidence, and enhancing market visibility.

While non-GMO and organic flours are often grouped together, they remain distinct categories. All organic flour is non-GMO, but non-GMO flour may still be grown using synthetic fertilizers or pesticides unless certified organic. This distinction has enabled non-GMO flour to appeal to a broader consumer base seeking transparency and affordability without fully committing to organic price premiums.

Key Growth Drivers Shaping the Market

One of the primary drivers of the non-GMO flour market is the global rise of clean-label food trends. Consumers increasingly associate non-GMO products with health, safety, and natural food systems, making them a preferred option for everyday cooking, baking, and food processing.

The expanding organic and natural food sector has indirectly boosted non-GMO flour demand, as both categories share common values around sustainability and ingredient purity. In addition, the growth of plant-based, gluten-free, keto, and specialty diets has significantly increased demand for diverse non-GMO flour alternatives, including almond, chickpea, lentil, rice, and specialty grain flours.

Another contributing factor is the resurgence of home baking and artisanal cooking, particularly in developed markets. Consumers are increasingly willing to pay a premium for high-quality, transparent ingredients, further supporting the growth of certified non-GMO flour products.

Market Challenges and Constraints

Despite favorable demand dynamics, the non-GMO flour market faces several operational challenges. Maintaining non-GMO integrity throughout the supply chain requires strict identity preservation, segregation, testing, and documentation, which increases production and logistics costs. These factors often translate into higher retail prices, limiting adoption in price-sensitive markets.

Additionally, limited awareness around GMO versus non-GMO distinctions in developing regions restricts broader market penetration. Smaller producers may also face difficulties complying with certification and documentation requirements, which can hinder market entry and scalability.

Regional and Country-Level Trends

North America represents the largest and most mature market for non-GMO flour, driven by high consumer awareness, established certification frameworks, and widespread availability across retail channels. Private-label non-GMO flours are increasingly common in supermarkets and health food stores.

In Europe, strong regulatory controls on genetically modified organisms and a well-established artisan baking culture support steady market growth. Countries such as Germany, France, and the Netherlands lead regional demand for non-GMO and heritage grain flours.

The Asia-Pacific region is experiencing gradual growth, particularly in urban centers, supported by rising disposable incomes, Western-style baking trends, and expanding health food retail in countries like Japan, South Korea, and Australia. Meanwhile, Latin America and the Middle East & Africa remain emerging markets, with adoption driven by premium imports, labeling transparency initiatives, and growing health awareness.

Competitive Landscape and Recent Developments

The non-GMO flour market is moderately fragmented, with competition centered on product quality, certification credibility, sourcing transparency, and alignment with dietary trends. Leading players differentiate through gluten-free offerings, specialty blends, sustainable packaging, and consumer education initiatives.

Recent product launches highlight continued innovation in the sector. In January 2025, Maskal Teff introduced certified organic, non-GMO brown teff flour at the Winter Fancy Food Show, while Nature’s Path Foods expanded its non-GMO flour portfolio in October 2024 with all-purpose, gluten-free, keto, and whole wheat variants.

Outlook

As clean-label consumption continues to reshape global food markets, non-GMO flour is expected to remain a key growth category. Companies that invest in certification, supply chain transparency, and consumer engagement will be best positioned to capture long-term opportunities in this evolving market.

Our Latest Publication

Non-GMO Flour Market Size Estimation, Share & Future Growth Trends Analysis, By Source (Flour Type) (Wheat Flour, Corn Flour / Maize Flour, Rice Flour (White Rice Flour, Brown Rice Flour), Almond Flour, Chickpea Flour, Lentil Flour, Pea Flour, Barley Flour, Oat Flour, Rye Flour, Specialty Flours, Others), By Form, By Nature, By End Use and Regional Analysis, 2026-2035

Our Latest News:

Companion Animal Diagnostics Market Set for Strong Growth Through 2035 Amid Rising Pet Healthcare Demand

Adarsh

Business Strategy — Quintile Reports

Adarsh is a Business Strategy professional focused on transforming market insights into actionable growth plans. He supports strategic initiatives through market analysis, competitive intelligence, and data-driven decision-making to help drive long-term business success.

His core skills include strategic planning, market research, growth opportunity assessment, trend analysis, performance tracking, stakeholder communication, cross-functional collaboration, and critical problem-solving.